After a challenging few years, European fintech funding is finally showing signs of recovery. The sector secured €3.6 billion in the first half of 2025, representing a 23% increase compared to the same period in 2024. While these figures remain well below the record-breaking levels of 2021 and 2022, investor confidence is gradually returning as startups shift towards sustainable growth strategies and clearer paths to profitability.

The landscape of European fintech funding has changed dramatically. Gone are the days when companies could raise massive rounds based purely on user growth projections. Today’s investors want to see lean operations, strong unit economics, and realistic revenue models. This article breaks down where the money is going, which cities and sectors are attracting capital, and what trends are shaping the future of financial technology across Europe.

The Current State of European Fintech Investment

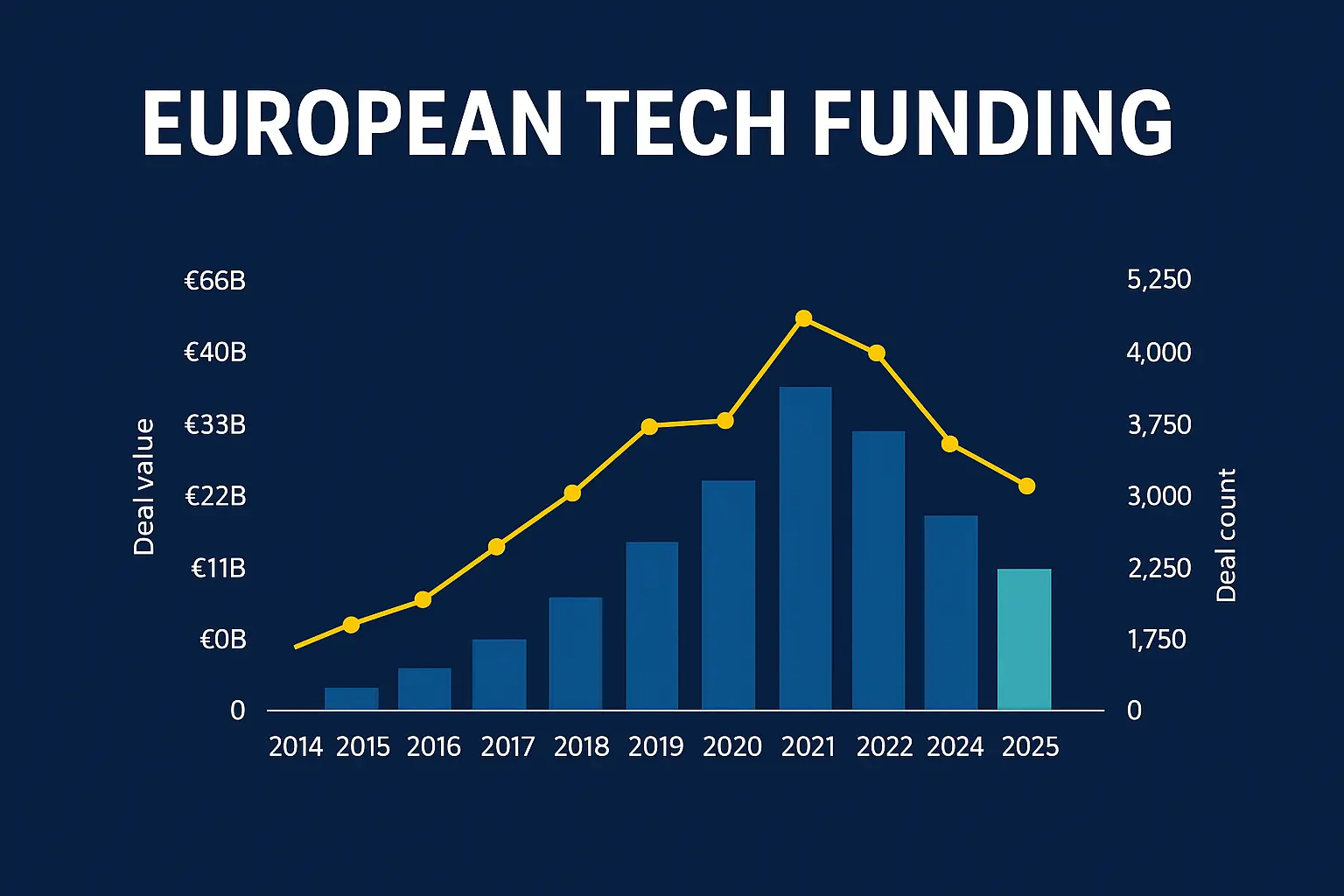

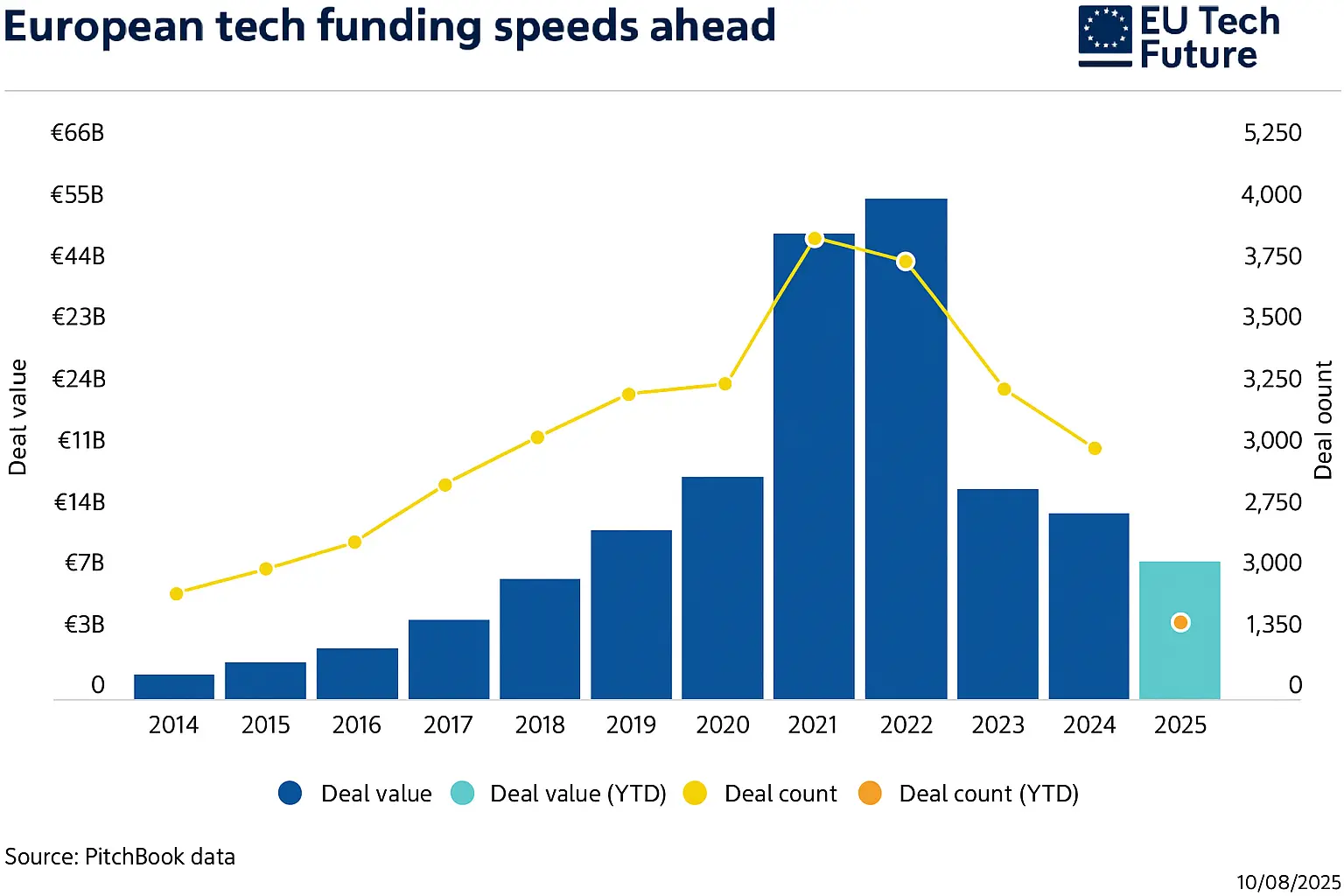

European fintech funding reached €6.3 billion throughout 2025, with over 70% of that total secured in the first half of the year. This represents a significant improvement from the cautious investment climate that dominated 2023 and 2024. The sector now accounts for 23% of all European venture capital funding, up from just 18% in the first half of 2024.

According to Finch Capital’s latest report, this recovery reflects not just improved market conditions, but also a fundamental shift in how fintech companies operate. Lower interest rates and easing inflation have certainly helped, but the bigger change lies in company building philosophy. Modern fintech startups prioritise capital efficiency, focus on revenue generation from day one, and build products designed for long-term sustainability rather than rapid scale at any cost.

How the UK Dominates European Fintech Funding

The United Kingdom captured an impressive 56% of total European fintech funding in the first half of 2025. Even more striking is that 79% of UK fintech investment is concentrated in London alone. This dominance isn’t accidental – London has established itself as Europe’s undisputed fintech capital through a combination of regulatory support, deep talent pools, and the presence of successful homegrown companies like Revolut and Monzo.

What sets the UK apart from other European markets is the diversity of its funding landscape. Unlike Germany and France, where one or two large deals can dominate the statistics, the UK shows a more balanced distribution of capital across multiple companies and sectors. London’s top two deals constitute less than 50% of total funding, demonstrating a mature ecosystem with opportunities across various fintech verticals.

The city benefits from what researchers call “founder factories” – successful fintech unicorns whose former employees go on to launch new startups. In London, 68% of fintech spinouts founded by ex-unicorn employees remain in the same city, creating a self-reinforcing cycle of talent, experience, and capital.

Why European Fintech Funding Declined (2021-2024)

To understand the 2025 recovery, you need to look back at what caused the slowdown. In the first half of 2022, European fintechs raised a staggering €15.3 billion. By H1 2024, that figure had plummeted to just €2.9 billion – an 81% decline. This wasn’t unique to fintech or Europe; it reflected a global recalibration of technology valuations.

Several factors contributed to this correction. Rising interest rates made capital more expensive and investors more selective. High inflation squeezed consumer spending, impacting B2C fintech models particularly hard. Perhaps most importantly, the market rejected the “growth at all costs” mentality that had dominated the 2020-2021 period.

Companies that had raised substantial rounds based on user acquisition metrics suddenly faced questions about profitability timelines. Many burned through capital trying to maintain growth rates, only to find that subsequent funding rounds either didn’t materialise or came at significantly reduced valuations. The European Central Bank’s analysis of fintech growth patterns highlighted how quickly market sentiment can shift when macro-economic conditions change.

Key Investment Trends Shaping European Fintech in 2025

B2B Fintech Continues to Attract Capital

Business-to-business fintech models have emerged as the clear winners in the current investment climate. B2B fintechs attracted 41% of all fintech venture capital in 2024 and that trend has continued into 2025. Investors prefer B2B models because they typically offer more predictable revenue streams, longer customer relationships, and higher switching costs than consumer-focused alternatives.

For founders building in the space, particularly those connected with platforms like EUTech, this represents both an opportunity and a competitive landscape. B2B fintech companies working in payments infrastructure, CFO tools, and embedded finance solutions are particularly well-positioned to secure funding.

AI-Driven Financial Tools Gain Investor Attention

Artificial intelligence represents 21% of European fintech deal volume in the first half of 2025, up from 16% the previous year. However, these deals account for just 7% of total deal value, suggesting that most AI-focused fintechs remain in earlier funding stages.

The way companies are deploying AI has changed significantly. Rather than building proprietary large language models from scratch, an expensive and resource-intensive process – most fintechs are now using existing models and customising them for specific financial services applications. This has led to a dramatic shift in hiring patterns, with demand for prompt engineers and integration specialists far exceeding that for traditional machine learning researchers.

One partner at a leading European VC firm noted that engineering team growth at top fintech companies has slowed from 20% in 2022 to an expected 2% by the end of 2025. This isn’t because companies are shrinking, rather, they’re optimising existing systems and focusing on integration rather than building new infrastructure.

Embedded Finance and Vertical Solutions

Embedded finance, the integration of financial services into non-financial platforms, continues to attract significant investment. Companies that can offer lending, payments, or insurance products directly within existing customer workflows are particularly attractive to investors. This trend is especially strong in vertical markets like logistics, manufacturing, and healthcare, where industry-specific fintech solutions can command premium pricing.

Virtual IBANs (International Bank Account Numbers) are being rapidly adopted to streamline payment collection and reconciliation. These tools assign unique identifiers to different payees while linking them all to a single master account, making financial operations significantly more efficient for businesses handling multiple payment streams.

Top Fintech Sectors Receiving European Funding

Alternative Lending and Credit Solutions

Alternative lending platforms attracted $8.1 billion globally in 2024, making it the single largest funded fintech category. These companies use technology to assess creditworthiness in ways traditional banks cannot, opening up lending opportunities for underserved market segments. European platforms in this space have been particularly successful at securing late-stage funding rounds.

Payment Processing and Digital Wallets

The payments sector remains consistently popular with investors, having received $141.1 billion in venture capital between 2016 and 2024, more than any other fintech sub-industry. In 2024 alone, payments companies secured $4.4 billion in funding. The sector’s enduring appeal lies in its fundamental role in the financial system and its relevance across both B2B and B2C markets.

London’s rich payments ecosystem has been a major driver of the UK’s dominance in European fintech funding. From payment gateways to cross-border transfer platforms, British companies have established themselves as category leaders.

CFO Tools and Financial Operations Software

Chief Financial Officer tools attracted $4.3 billion in global funding during 2024. These platforms help businesses automate financial planning, expense management, treasury operations, and regulatory reporting. As companies face increasing pressure to demonstrate financial discipline, software that improves visibility and control over cash flow has become highly valued.

Leading European Cities for Fintech Investment

Beyond London’s clear dominance, several other European cities have established themselves as significant fintech hubs. Stockholm hosts four unicorn founder factories that have spawned 96 fintech spinouts. Paris boasts 10 unicorn founder factories with 70 spinouts, and notably, 79% of these spinouts chose to remain in Paris, the highest retention rate of any major European city.

Berlin’s seven unicorn founder factories have generated 67 spinouts, while Amsterdam’s five founder factories have produced 37 new companies. Each city offers different advantages: Berlin provides access to deep technical talent, Paris offers proximity to major European financial institutions, and Amsterdam serves as a strategic location for companies targeting both UK and continental European markets.

Germany’s median deal value increased by 189% year-on-year, though its total deal count of 27 lags behind France’s 38 deals. This suggests that while German fintech companies can secure substantial funding rounds, the ecosystem hasn’t yet achieved the breadth of the UK or French markets.

Notable European VC Funds Backing Fintech Startups

The European fintech investment landscape includes both generalist technology investors and specialist fintech funds. Earlybird Venture Capital, based in Germany, backs startups across Europe from early to growth stages, with particular interest in fintech infrastructure and wealth management technology. Sweden’s EQT Ventures operates as a multi-stage fund with offices across Europe and San Francisco, supporting tech startups including financial technology companies.

Regional specialists play an increasingly important role. Bulgaria’s Eleven Ventures focuses specifically on Central and Eastern European fintechs, providing not just capital but also critical support in accessing cross-border markets. Poland and US-based FF Venture Capital takes a hands-on operational approach with early-stage fintech companies working in automation, cybersecurity, and AI.

For companies working with digital assets and blockchain technology, Switzerland’s Laser Digital – backed by global financial group Nomura, provides both capital and strategic connections to traditional financial institutions. Austria’s Speedinvest offers pan-European investment from pre-seed through Series B stages, with dedicated fintech expertise.

EU Regulations Impacting Fintech Investment

Regulatory changes scheduled between 2025 and 2027 are significantly shaping investment decisions. The Digital Operational Resilience Act (DORA) requires financial institutions and technology service providers to strengthen their cybersecurity and operational resilience. This has created opportunities for regtech companies offering compliance solutions.

Payment Services Directive 3 (PSD3) represents the next evolution of open banking regulation. The directive aims to increase consumer protection while facilitating greater data sharing between financial institutions. Companies building infrastructure to support open banking are attracting substantial investment based on the anticipated regulatory requirements.

The European Digital Identity (EUDI) framework and updated eIDAS regulation will impact how fintech companies verify customer identities and manage digital signatures. According to the European Commission, these changes are designed to create seamless cross-border digital services while maintaining high security standards.

E-invoicing mandates and the Consumer Credit Directive 2 (CCD2) round out the regulatory agenda. While compliance requires investment, these regulations also level the playing field between traditional banks and fintech challengers, potentially opening up new market opportunities.

What Investors Look for in European Fintech Startups

Today’s European fintech funding environment rewards different characteristics than the 2021 boom period. Investors prioritise companies with lean operations that can demonstrate efficient customer acquisition costs and strong unit economics. A clear path to profitability matters more than aggressive growth projections.

Defensible business models have become critical. Whether through network effects, regulatory moats, or proprietary technology, startups need to articulate why they won’t be immediately undermined by competitors or disintermediated by incumbent financial institutions. This is particularly important in crowded categories like payments and lending.

Revenue diversification has also gained importance. Companies that rely on a single revenue stream or a small number of large customers face greater scrutiny than those with diversified income sources. This reflects lessons learned during the 2023-2024 downturn, when some well-funded fintechs collapsed rapidly after losing key partnerships or revenue channels.

Future Outlook for European Fintech Funding

The trajectory for the remainder of 2025 and into 2026 appears cautiously optimistic. If current trends continue, European fintech funding for the full year 2025 could reach €8-9 billion, still well below the peak years but representing a solid recovery from the 2024 low point.

AI integration will continue driving investment, though the focus will shift from building foundational models to developing specific financial services applications. Expect to see more deals in areas like AI-powered fraud detection, personalised financial advisory services, and automated regulatory compliance.

Geographic expansion within Europe presents opportunities. While the UK, Germany, and France dominate current funding statistics, investors are increasingly looking at promising companies in Portugal, the Netherlands, Romania, and the Nordics. These markets often offer strong technical talent at lower costs and growing domestic markets for fintech services.

Open banking‘s continued expansion under PSD3 will create opportunities for companies building data aggregation infrastructure, consent management platforms, and consumer-facing applications that leverage multi-bank data. The Wikipedia article on open banking provides useful context on how this regulatory framework is reshaping financial services.

What to Expect from EU Tech Funding in 2026

Looking ahead to 2026, European tech funding is positioned for continued growth, driven by several converging factors. Consumer usage of generative AI is expected to double across most European countries in 2026, creating significant opportunities for fintech startups that can integrate AI-powered features into financial products. However, enterprise adoption of AI in Europe will likely lag behind the United States, meaning consumer-facing fintech applications may see stronger funding than purely B2B infrastructure plays.

One particularly noteworthy trend is the surge in defence and critical infrastructure spending. Public-sector bodies and critical infrastructure operators are predicted to see tech budgets rise by 20% in 2026, which will have knock-on effects for fintech companies serving government clients or working in areas like digital identity verification, secure payment systems, and fraud prevention for public services.

The Green Fintech Movement Gains Momentum

Perhaps the most compelling fact-based trend for 2026 is the explosive growth of green fintech. The global green fintech market is projected to grow at a compound annual growth rate of 22.4% until 2029, positioning sustainable finance technology as one of the fastest-growing segments within the broader fintech ecosystem.

Green fintech encompasses companies working on carbon credit marketplaces, ESG (Environmental, Social, and Governance) data platforms, sustainable investment tools, and digital lending platforms that offer preferential rates for clean energy projects and electric vehicle purchases. This segment appeals to investors because it combines strong growth potential with positive social impact – a rare combination in today’s market.

For European founders, particularly those working within networks like EUTech, green fintech represents an opportunity to tap into both venture capital interest and supportive regulatory frameworks. The European Union’s commitment to reaching net-zero emissions by 2050 means that fintech solutions supporting this transition will likely benefit from both funding and policy support.

Digital Sovereignty Without Abandonment

Another key trend shaping 2026 will be Europe’s continued push for digital sovereignty – the ability to control its own technology infrastructure and data, without completely abandoning established US technology providers. European firms will accelerate efforts for digital sovereignty but won’t fully abandon US hyperscalers in 2026, leaving AWS, Microsoft Azure, and Google Cloud dominant.

For fintech companies, this means that building on existing cloud infrastructure remains viable, but there’s growing opportunity for startups that can provide European alternatives or hybrid solutions that balance functionality with data sovereignty requirements. Payment processing infrastructure, banking-as-a-service platforms, and financial data storage solutions built specifically for EU regulatory compliance will be particularly attractive to investors.

Venture Capital Growth Projections

Global venture capital investment is forecast to grow at approximately 16% annually through 2026, according to market research. While this represents an optimistic scenario, it suggests that the funding environment will continue improving from the 2023-2024 lows. For European fintech specifically, this could translate to annual funding levels reaching €10-12 billion by 2026, approaching pre-correction levels but with a much healthier focus on sustainable business models.

The key difference between the upcoming funding cycle and the 2021 boom is the quality of capital deployment. Investors in 2026 will prioritise companies with proven revenue models, clear paths to profitability, and defensible competitive positions. The “spray and pray” approach of the early 2020s has been replaced by rigorous due diligence and expectation of near-term financial discipline.

Frequently Asked Questions

Which country leads European fintech funding?

The United Kingdom captured 56% of total European fintech funding in H1 2025, with 79% of that concentrated in London. Germany and France are distant second and third places.

What fintech sectors attract the most investment?

Alternative lending and credit ($8.1B globally in 2024), payments ($4.4B), and CFO tools ($4.3B) were the top three funded fintech sectors. B2B fintech models generally attract more capital than B2C.

Why is B2B fintech more attractive than B2C?

B2B fintech offers more predictable revenue streams, longer customer relationships, higher switching costs, and typically requires less capital to achieve profitability compared to consumer-focused models.

How is AI changing European fintech investment?

AI-focused fintechs now represent 21% of deal volume in European fintech. However, companies are focusing on integrating existing AI models rather than building proprietary systems, leading to changes in hiring patterns and resource allocation.

What regulations are affecting European fintech in 2025?

Key regulations include DORA (operational resilience), PSD3 (open banking evolution), eIDAS updates (digital identity), e-invoicing mandates, and Consumer Credit Directive 2. These are scheduled for implementation between 2025 and 2027.

Looking to connect with Europe’s fintech ecosystem? Discover the latest funding rounds, startup showcases, and investor networks through European fintech funding initiatives and fintech startup ecosystems across the EU. Stay updated on venture capital trends in European tech, AI integration in European financial services, B2B fintech investment opportunities, London fintech hub developments, and European payments sector innovation.

Author: Ujwal Krishnan

Ujwal Krishnan is an AI and SEO specialist dedicated to helping UK businesses navigate and strategize within the ever-evolving AI landscape. With a Master's degree in Digital Marketing from Northumbria University, a degree in Political Science, and a diploma in Mass Communication, Ujwal brings a unique interdisciplinary perspective to the intersection of technology, business, and communication. He is a keen researcher and avid reader on deep tech, AI, and related innovations across Europe, informed by their valuable experience working with leading deep tech venture capital firms in the region.