The global healthcare landscape is currently undergoing a profound transformation, driven not by new surgical techniques or pharmacological breakthroughs alone, but by a quieter, yet arguably more pervasive force: technology. In recent years, we’ve seen a monumental shift from reactive ‘sick-care’ to proactive ‘health-care’, largely thanks to the innovation delivered by thousands of digital health firms worldwide.

For anyone tracking the intersection of technology and wellbeing, understanding the modern health tech companies that are leading this change is essential. These enterprises are revolutionising everything from how a complex drug is discovered to how you book a virtual consultation with your GP. It is a market that is not just growing, but exploding, marking digital healthcare as one of the most critical sectors of the next decade.

What are Health Tech Companies? Defining the Digital Health Ecosystem

A health tech company is an enterprise that leverages digital technology, software, and data science to improve the delivery, payment, or consumption of healthcare services. Unlike traditional medical equipment manufacturers, these firms focus primarily on the digital infrastructure that enables, enhances, or optimises patient care, medical processes, and preventative health management. Simply put, if it runs on code, uses data, or connects people virtually to care, it falls under the health tech banner.

This sector has rapidly matured, moving beyond simple fitness apps to deliver sophisticated, clinical-grade solutions. The core mandate of most health tech firms is to address systemic inefficiencies, enhance patient access, reduce costs, and, crucially, empower individuals to manage their own health proactively.

Healthtech vs. Medtech: Where the Line is Drawn

The terms ‘health tech’ and ‘medtech’ are often used interchangeably, but there is an important distinction.

- MedTech (Medical Technology) generally refers to the use of physical, often regulated, devices and equipment used primarily in clinical settings. This includes MRI scanners, surgical robots, innovative implants, and diagnostic tools used on the patient during a procedure or hospital stay. These products typically require lengthy and rigorous regulatory approval cycles from bodies like the MHRA or FDA.

- Health tech, or digital health, focuses on software, services, and data management. Think of applications, platforms, data analytics tools, and remote monitoring systems. While some health tech solutions involve hardware (like smart scales or specific wearables), their primary value lies in the software and data insights they generate. Health tech is often consumer-facing or provides administrative support, whereas medtech is typically clinician-facing and procedure-based.

The Engine Room of Change: Primary Focus Areas for Health Tech Companies

The immense valuation of the digital health market stems from the sheer breadth of problems health tech companies are tackling. From the lab bench to the living room, the sector can be broadly categorised by the primary function it serves.

AI, Machine Learning, and Precision Drug Discovery

Perhaps the most transformative area is the application of Artificial Intelligence (AI) and machine learning (ML) in early-stage research. Companies in this segment are using vast datasets—including genomics, real-world evidence, and historical trial data, to significantly accelerate the time it takes to identify a novel drug candidate.

AI models can predict a molecule’s potency, identify previously overlooked drug targets for rare diseases, and even automate the design of small-molecule drugs. Firms like Exscientia and Benevolent AI are prime examples of this computational approach, where algorithms replace years of costly lab work, promising quicker access to complex therapies. This not only lowers the financial barrier for pharmaceutical development but fundamentally changes the timeline for treating critical illnesses.

Telehealth and Remote Patient Monitoring (RPM)

The COVID-19 pandemic permanently normalised remote access to care. Telehealth and RPM health tech companies build the platforms that connect patients with clinicians virtually, often through video consultations or messaging. This increases accessibility, particularly in rural or underserved areas, and dramatically reduces hospital wait times.

RPM platforms, such as those offered by Huma, involve wearable devices or digital tools that continuously track a patient’s vital signs, activity, and symptoms from home. AI then analyses this stream of data, flagging anomalies to healthcare providers for early intervention. For managing chronic conditions like diabetes, heart failure, or respiratory diseases, RPM is invaluable, leading to fewer expensive hospital admissions and enabling faster clinical decisions.

Administrative Efficiency (Provider Operations)

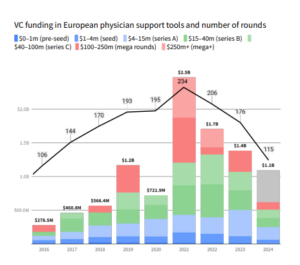

One of the largest drains on healthcare resources is bureaucracy. Data from 2024 and 2025 shows a significant shift in venture capital funding towards solutions for provider operations, capturing approximately 44% of all health tech investment.

This area involves software-as-a-service (SaaS) and AI tools designed to streamline the colossal administrative burden faced by hospitals and general practice surgeries. This includes automated patient scheduling, AI-powered systems for reducing billing errors, predictive staffing models, and digitising medical records (Electronic Health Records or EHRs) to ensure data interoperability. By automating routine, non-clinical tasks, these health tech companies free up nurses and doctors to focus on patient care, directly addressing issues like staff burnout and soaring overheads. You can read more about how this technology is driving efficiency in our piece on AI in technology and business efficiency.

Mental Health and Digital Therapeutics (DTx)

As digital platforms become integrated into daily life, mental wellness and psychological support have become a major focus. Health tech companies in this space offer platforms like Unmind, which provide preventative mental health resources for employees, or specific applications that deliver therapy.

Digital Therapeutics (DTx) are a particularly exciting sub-segment. These are software programs designed to treat, manage, or prevent a disease or disorder, often prescribed by a doctor alongside or instead of medication. For instance, DTx are now used for managing chronic insomnia, controlling symptoms of COPD, or supporting individuals with addiction. Unlike consumer apps, DTx products require clinical validation and regulatory oversight, effectively turning software into medicine.

Read more: Cleantech Europe: Investment, Innovation & Policy 2025

Explosive Growth: Global Investment Trends in Healthcare Technology

The growth trajectory of digital healthcare is nothing short of phenomenal. The global digital health market was valued at approximately $427 billion in 2025 and is projected to accelerate at a Compound Annual Growth Rate (CAGR) exceeding 20% over the subsequent years. This puts the sector on a path to reach well over $1 trillion by the early 2030s.

The surge in investment, particularly following the rapid adoption of digital tools during the pandemic, underscores the market’s maturity and investor confidence. While the United States remains the largest market, regions like Europe and Asia-Pacific are catching up rapidly, driven by national digital transformation agendas.

The UK market itself has mirrored this global trend, with investment figures consistently reaching new records year-on-year, demonstrating a strong pipeline of innovative health tech companies operating within the European ecosystem. This blend of public sector demand (like the NHS’s ongoing digitalisation plans) and strong private investment provides a fertile ground for these healthcare technology firms to scale their solutions globally.

The shift in venture capital focus is perhaps the most revealing metric: away from experimental direct-to-consumer models and towards solutions that deliver clear, measurable Return on Investment (ROI) for major healthcare providers and payers. This movement ensures that the technology being developed is not just novel, but practical and scalable, directly addressing the cost crisis in healthcare.

Also Read: Healthtech Companies UK

The 2025 Forecast: Key Trends Shaping the Future of Health Tech

Looking ahead to the rest of 2025 and beyond, three core trends are defining the strategic direction of leading health tech companies.

Genomics and Pharmacogenomics: Truly Personalised Medicine

The future of healthcare is moving decisively towards personalisation, and genomics is the cornerstone of this shift. Genomics studies the role of genes and their impact on health, allowing for proactive risk mitigation. Pharmacogenomics, specifically, examines how an individual’s DNA affects their response to drugs.

Health tech companies are deploying AI to integrate genomic data with clinical records, enabling clinicians to tailor medication dosage, select more effective drugs, and predict adverse reactions based on a patient’s unique genetic profile. This is moving medicine from a ‘one-size-fits-all’ approach to precision treatment, promising far better outcomes and significantly reduced systemic wastage. This level of data management and analysis relies heavily on robust data privacy and management in tech strategies.

Decentralisation of Care and the ‘Digital Front Door’

Healthcare is fundamentally moving out of the hospital and into the home. This decentralisation is being facilitated by RPM and mobile-based services, making care more convenient and reducing the strain on centralised facilities. The concept of the ‘digital front door’ is crucial here.

This refers to a single, centralised digital point of access where a patient can manage appointments, view records, conduct virtual visits, receive test results, and monitor their health data. This seamless, consumer-grade experience is becoming the competitive standard among health tech companies that partner with major healthcare systems, turning complex administrative tasks into simple digital interactions.

The Rise of Consumer-Led Wellness (Wearables and mHealth)

While consumer-grade wearables (smartwatches and fitness trackers) aren’t clinical-grade, they are generating massive amounts of physiological data. Health tech companies are finding increasingly clever ways to leverage this data for preventative models.

The mHealth (mobile health) segment, which includes apps and health trackers, is growing rapidly, fueled by rising health consciousness and the widespread use of mobile platforms. When combined with professional oversight (such as home-based blood testing services or personalised nutrition apps like ZOE), this consumer data becomes actionable, promoting better lifestyle choices and identifying potential health issues long before they become emergencies.

The Hurdles Ahead: Key Challenges for Health Tech Companies in Europe

Despite the immense momentum, the sector faces several significant roadblocks, particularly within the fragmented European market. Successfully navigating these challenges will separate the pioneering health tech companies from those that fail to scale.

Navigating Regulatory Landscapes and Data Sovereignty (GDPR)

One of the greatest challenges is harmonising innovation with the complex regulatory environment. Unlike a single market like the US, operating across Europe means complying with diverse national health service requirements and, crucially, the rigorous standards of the General Data Protection Regulation (GDPR).

GDPR demands stringent data handling protocols, especially for sensitive health information, requiring firms to invest heavily in robust cybersecurity and governance frameworks. While necessary for patient protection, these complex, multi-jurisdictional compliance requirements can slow down market entry and increase the cost of scaling new digital health solutions across the continent. This is a perpetual challenge facing European tech and regulatory compliance.

System Integration and Workforce Skills Gap

Implementing new technologies within legacy healthcare systems is often cited as a major operational obstacle. Many hospitals and GP surgeries still rely on decades-old IT infrastructure that struggles to integrate seamlessly with modern cloud-based health tech platforms. Overcoming this requires extensive bespoke integration work and significant political willpower.

Furthermore, there is a clear skills shortage. The digital health ecosystem requires a rare blend of clinical knowledge, data science expertise, and robust cybersecurity skills. Finding and retaining staff capable of building, managing, and operating these sophisticated systems—from AI developers to clinical informaticians—remains a major constraint on growth.

Building Trust and Addressing the Digital Divide

Finally, widespread adoption hinges on trust. Clinicians must trust that the new technology provides accurate, actionable insights, and patients must trust that their sensitive data is secure and that the technology genuinely improves their care, rather than acting as a barrier.

We must also consider the digital divide. As care becomes decentralised and access moves online, there is a risk of excluding older populations, low-income groups, or those with limited digital literacy. The most successful health tech companies are those that design their solutions with universal accessibility and strong, empathetic clinician involvement at the core of their development process.

Conclusion

The future of healthcare is undeniably digital. Health tech companies are no longer peripheral players; they are the central architects of a system that is rapidly shifting towards being patient-centric, preventative, and personalised.

From AI-powered drug discovery to the seamless delivery of care via telehealth platforms, these digital innovations are providing the critical tools needed to manage chronic diseases, reduce operational waste, and ultimately deliver better health outcomes for populations across the globe.

While challenges around regulation and integration persist, the momentum created by soaring investment and urgent public demand guarantees that the healthcare technology sector will continue its explosive trajectory. Understanding and investing in these disruptive forces is key to building a sustainable and resilient healthcare system for the future. For more insights into the future of medicine, be sure to check out our analysis on biotech innovation and the future of medicine.