If you’ve been scrolling through TikTok or checking your LinkedIn feed recently, you might have noticed something alarming: countless posts suggesting that Klarna, the Swedish buy now, pay later giant, is about to collapse. With millions of views and creators encouraging users to stop paying their debts, the rumour mill has gone into overdrive.

But is there any truth to these claims? Let’s separate the viral speculation from the financial facts.

Why Are People Saying Klarna Is Going Bankrupt?

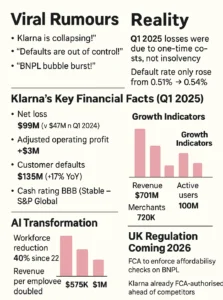

The bankruptcy rumours started gaining serious traction after Klarna released its Q1 2025 earnings report in mid-May. The numbers looked concerning at first glance: a net loss of $99 million, more than double the $47 million loss from the same period last year. Customer defaults also rose by 17% year-over-year to reach $136 million.

For a company built on lending money to consumers, these figures naturally raised eyebrows. Social media amplified the concern, with TikTok videos racking up over 5 million views and some creators even positioning non-payment as a form of protest against “predatory BNPL practices.”

The narrative seemed to fit perfectly: a fintech unicorn weakened by unpaid loans and a delayed IPO finally crumbling under its own business model. However, the reality is significantly more complex.

Understanding Klarna’s Q1 2025 Financial Report

When you look beyond the headline numbers, Klarna’s financial situation tells a different story. Yes, the company reported a $99 million net loss, but this wasn’t purely from customers not paying back their loans.

A substantial portion of that loss came from one-time costs: share-based compensation related to the paused IPO, restructuring expenses, and depreciation charges. Strip away these exceptional items, and Klarna actually posted an adjusted operating profit of $3 million for the quarter. That’s hardly the picture of a company on the brink of collapse.

The 17% increase in customer defaults also needs context. Klarna’s loan portfolio has grown substantially, meaning more customers and more transactions naturally lead to higher absolute default numbers. The crucial metric is the default rate, which has remained remarkably stable, rising only from 0.51% to 0.54% over the past year.

To put this in perspective, traditional credit cards typically see default rates between 2.5% and 3.5%. Klarna’s 0.54% rate is significantly lower, largely because their loans are short-term and small-value. The company reports that 83% of its loan portfolio turns over within 90 days, allowing for quick risk model adjustments.

Klarna’s Credit Rating Tells a Different Story

Klarna is not bankrupt. Because, if Klarna were genuinely heading towards bankruptcy, credit rating agencies would be sounding the alarm. Instead, S&P Global reaffirmed Klarna’s BBB rating in April 2025, maintaining a stable outlook.

This investment-grade rating matches established banks like Spain’s Banco Sabadell. S&P’s assessment reflects confidence in Klarna’s solid liquidity position, with $10.4 billion in cash reserves, and their belief in the company’s future profitability despite current economic challenges.

For context, when UK payday lender Wonga collapsed in 2018, warning signs appeared months in advance through deteriorating credit assessments and regulatory interventions. Klarna’s situation shows none of these red flags. The company’s financial resilience mirrors patterns seen in successful deep tech companies in Europe that weather market volatility through strong fundamentals.

What’s Really Happening with Klarna’s IPO?

The IPO situation has added fuel to the bankruptcy speculation. Klarna filed for a US IPO in March 2025, seeking a valuation above $15 billion. However, they paused these plans in April when new US tariffs triggered market volatility.

Company insiders maintain this delay is purely strategic. Klarna’s leadership is waiting for better market conditions and stronger investor interest before going public. This isn’t unusual. Airbnb delayed its IPO in 2019, allowing early investors to sell shares through secondary markets, before successfully going public in 2020 with a much stronger valuation. For more insights on European venture capital funding patterns, these strategic delays often result in stronger valuations.

Klarna has adopted a similar approach, enabling early investors to sell shares pre-IPO through secondary markets. This helps stabilise the company’s valuation whilst gauging genuine market interest. CEO Sebastian Siemiatkowski is betting that AI-driven improvements and recovering tech valuations will create better conditions for the eventual public offering.

Growth Metrics That Counter the Bankruptcy Narrative

Whilst loss-making headlines grab attention, Klarna’s operational performance suggests a healthy, growing business. The company reported 13-15% year-over-year revenue growth, reaching $701 million in Q1 2025.

User numbers continue climbing, with 100 million active users representing an 18% increase from last year. The merchant network has expanded by 27% to over 720,000 partners, including major retailers like Walmart, DoorDash, and eBay.

Particularly impressive is Klarna’s US performance, showing 33% revenue growth. For a European company successfully scaling in the competitive American market, these numbers demonstrate genuine business momentum rather than a company in terminal decline. Competitors like Clearpay (Afterpay) and PayPal Pay in 4 also continue expanding in the BNPL space.

How AI Is Reshaping Klarna’s Business Model

Since 2022, Klarna has reduced its workforce by 40%, with artificial intelligence handling much of customer service and operations. This transformation has nearly doubled revenue per employee, from $575,000 to $1 million.

Whilst workforce reductions often signal trouble, in Klarna’s case this represents a deliberate shift towards an AI-first operating model. The company maintains human staff for complex customer interactions but uses automation for routine queries and risk assessment. This mirrors broader trends in AI-powered business transformation across European tech companies.

This efficiency drive helps explain how Klarna maintains profitability on an adjusted basis whilst still showing headline losses from restructuring costs. The company is essentially investing now for long-term operational efficiency, a strategy common among AI-focused startups in Europe.

The TikTok Factor: When Social Media Becomes a Business Risk

One genuinely concerning development is the social media-driven movement encouraging users to default on Klarna payments. Videos portraying non-payment as activism have garnered millions of views, with credit losses spiking notably among Gen Z users.

This represents a new type of business risk. If enough users lose confidence or deliberately default following social media trends, the negative narrative could become self-fulfilling. Klarna is responding by balancing AI cost-cutting with enhanced human customer service to manage these sensitive issues.

The company has also increased financial education initiatives and transparency efforts, though reputational damage may take time to repair.

UK Regulatory Changes: What’s Coming in 2026?

UK consumers should be aware of significant regulatory changes coming to the BNPL sector. The Financial Conduct Authority will implement mandatory oversight in 2026, including compulsory affordability checks before extending credit. Understanding how AI regulations like the EU AI Act shape fintech operations can provide context for these upcoming changes.

Klarna already holds FCA authorisation, giving them a head start over competitors as new regulations arrive. The company has also strategically sold Klarna Checkout for $520 million to focus on embedded finance, partnering with major retailers rather than managing checkout infrastructure.

These moves suggest forward planning rather than desperate asset sales. You can read more about fintech regulatory compliance at the FCA’s official website.

Should UK Consumers Worry About Using Klarna?

For UK consumers currently using Klarna, the bankruptcy concerns appear overblown. The company’s substantial cash reserves, investment-grade credit rating, and continued business growth suggest financial stability for the foreseeable future.

That said, responsible use of any credit product remains essential. Klarna and other BNPL services can be useful tools for managing cash flow on planned purchases, but they shouldn’t be used to fund spending beyond your means. Similar to how innovative payment technologies like Handwave are transforming transactions, BNPL represents the evolution of consumer finance.

If you’re concerned about digital payment innovations and their impact on personal finance, eutechfuture offers insights into emerging financial technologies and their practical implications for consumers and businesses.

The Verdict: Is Klarna Going Bankrupt?

Based on available evidence, Klarna is not going bankrupt. The company faces genuine challenges including rising credit losses, regulatory pressure, a delayed IPO, and reputational damage from social media speculation. However, these difficulties don’t amount to imminent financial collapse. Similar to how European startups navigate growth challenges, Klarna is adapting to market conditions whilst maintaining core business strength.

With $10.4 billion in cash reserves, a stable BBB credit rating, growing user numbers, and expanding revenue, Klarna has ample runway to weather difficult periods. The company’s success will depend on effective risk management, adapting to new regulations, and rebuilding market confidence ahead of an eventual IPO.

The real test for Klarna isn’t surviving the next few months, but whether it can successfully transform into an AI-powered financial platform whilst maintaining consumer trust. For broader context on BNPL industry dynamics, see the Buy Now, Pay Later. That’s a question about long-term strategy and execution, not short-term solvency.

FAQs About Klarna’s Financial Situation

What happens to my Klarna debt if the company goes bankrupt?

If Klarna were to face bankruptcy (which current evidence doesn't suggest), your debt wouldn't disappear. It would likely be sold to another financial institution or debt collection agency, and you'd remain legally obligated to repay it.

Why did Klarna pause its IPO?

Klarna launched its initial public offering (IPO) on the New York Stock Exchange (NYSE) in September 2025, raising approximately $1.37 billion by selling 34.3 million shares at $40 apiece, surpassing the anticipated price range and valuing the company at roughly $15 billion. The IPO was the largest of 2025 and drew significant oversubscription, with shares closing higher on their debut on the NYSE under the ticker symbol "KLAR".

How does Klarna's default rate compare to credit cards?

Klarna's default rate stands at 0.54%, significantly lower than the 2.5-3.5% typical for credit cards. This reflects the short-term, small-value nature of BNPL loans.

Is it safe to use Klarna right now?

Yes, Klarna remains safe to use. The company is financially stable with substantial reserves. However, as with any credit product, only use it for purchases you can afford to repay.

What's happening with BNPL regulation in the UK?

The FCA will implement mandatory oversight of BNPL services in 2026, including affordability checks. Klarna already holds FCA authorisation, positioning them well for these changes.

Did TikTok really hurt Klarna's finances?

Videos encouraging defaults have contributed to credit losses, particularly among Gen Z users. Whilst concerning, this represents a portion of Klarna's challenges rather than the primary cause of financial difficulties.

Stay Informed About Fintech Developments

The Klarna situation highlights how quickly misinformation can spread in the digital age, particularly regarding complex financial matters. Whether you’re a consumer trying to make informed decisions about payment methods or a business owner considering BNPL partnerships, understanding the facts behind the headlines is essential.

At eutechfuture, we break down complex technology and finance stories into clear, actionable insights. From AI-driven business transformations to regulatory changes affecting your industry, we help you stay ahead of developments that matter to your business and personal finances.

Want to understand how emerging technologies are reshaping finance, retail, and business operations? Visit EU Tech Future for in-depth analysis, practical guides, and expert perspectives on the innovations driving tomorrow’s economy.

Author: Ujwal Krishnan

Ujwal Krishnan is an AI and SEO specialist dedicated to helping UK businesses navigate and strategize within the ever-evolving AI landscape. With a Master's degree in Digital Marketing from Northumbria University, a degree in Political Science, and a diploma in Mass Communication, Ujwal brings a unique interdisciplinary perspective to the intersection of technology, business, and communication. He is a keen researcher and avid reader on deep tech, AI, and related innovations across Europe, informed by their valuable experience working with leading deep tech venture capital firms in the region.